Options for Fiat Liquidity: Comparing Bitcoin-Backed Loans and Digital Credit

Bitcoin holders often want to keep their Bitcoin intact while accessing fiat cash for living expenses, business operations, or other needs. Two established Bitcoin-native tools now make this possible without selling any sats: Bitcoin-backed loans and Digital Credit. This article provides a clear, side-by-side overview to help individuals and businesses evaluate which approach may better fit their situation, using the Variable Rate Series A Perpetual “Stretch” Preferred Stock issued by Strategy Inc. as the example for Digital Credit. This is an objective evaluation of options, not financial advice.

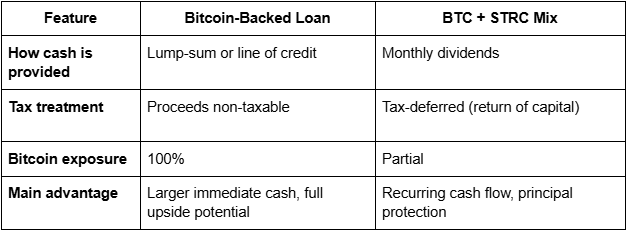

At a Glance

What Are Bitcoin-Backed Loans?

A Bitcoin-backed loan lets you borrow U.S. dollars by pledging your Bitcoin as collateral. You retain ownership of the Bitcoin, which continues to sit in your wallet or with a trusted custodian, and you receive cash upfront or through a line of credit. Interest is paid periodically. The cash proceeds from the loan are generally non-taxable because they represent borrowed funds rather than income.

What Is STRC?

STRC is perpetual preferred stock issued by Strategy Inc., a publicly traded company with the largest corporate Bitcoin treasury. When investors buy STRC, the company uses the proceeds to purchase additional Bitcoin. In return, holders receive monthly cash dividends and a security designed to trade near a stable par value of $100 per share through an adjustable dividend rate. The dividends are treated as return of capital (ROC) for tax purposes, which makes the cash flow tax-deferred until the shares are sold.

Both tools keep capital stored in Bitcoin while delivering usable fiat cash.

How the Strategies Are Structured

Bitcoin-backed loan

Allocation: 100 percent of capital into Bitcoin.

Typical terms: Conservative loan-to-value (LTV) ratio of 20 to 50 percent, interest rates between 9 and 12 percent APR (interest-only common).

Cash access: Lump-sum or revolving line of credit. Example: With $1 million invested in Bitcoin at $100,000 per coin, a 20 percent LTV loan provides $200,000 in cash. Annual interest at 10.5 percent equals roughly $21,000, for net cash of about $179,000. The cash received is non-taxable.

Repayment: The borrowed principal must be repaid or refinanced at maturity, typically after 12 to 36 months. This is usually handled with new cash inflows or by rolling the loan into a new facility. The principal remains a liability on the portfolio until repaid, requiring ongoing management but avoiding any forced sale of Bitcoin if the borrower plans accordingly.

BTC + STRC mix

Allocation: Majority in direct Bitcoin plus a portion in STRC. 75 percent Bitcoin and 25 percent STRC is a balanced starting point for those looking for a majority Bitcoin-only portfolio.

Typical terms: STRC currently pays an 11.5 percent annualized dividend, distributed monthly in cash. Shares are structured to maintain price stability near $100. With $250,000 allocated to STRC, annual cash flow equals approximately $28,750. The dividends are treated as return of capital, providing tax-deferred cash flow. The remaining $750,000 buys 7.5 Bitcoin. Allocations can be adjusted higher toward STRC when greater cash flow is the priority.

Key Risks of Each Approach

Bitcoin-backed loans carry interest costs that reduce net cash received, liquidation risk if Bitcoin falls sharply and breaches the LTV threshold, repayment or refinancing risk at maturity, and counterparty risk with the lending platform or custodian. While loan proceeds are non-taxable, the interest expense is generally not deductible for personal borrowing.

STRC carries dividend variability (the rate can adjust), issuer credit risk tied to Strategy Inc., potential principal fluctuations due to market conditions, and lower overall Bitcoin price upside because part of the capital is in the preferred stock rather than direct Bitcoin. Both strategies involve counterparty exposure, but each is backed by Bitcoin holdings in different ways. The tax-deferred nature of STRC dividends provides an advantage for many holders.

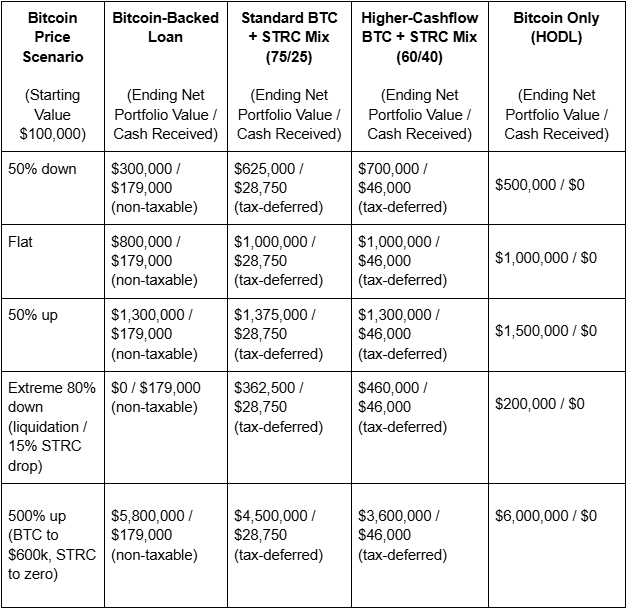

One-Year Performance Scenarios

Assume an investor or business starts with $1 million and Bitcoin priced at $100,000. Cash received is spent on expenses in all cases. We compare five Bitcoin price paths after one year: a 50 percent decline (to $50,000), flat (remains $100,000), a 50 percent increase (to $150,000), an extreme 80 percent drawdown (to $20,000) that triggers loan liquidation and a 15 percent decline in STRC value, and a 500 percent Bitcoin rally (to $600,000) in which for whatever hypothetical reason STRC collapses to zero and all liquidation capital is paid to more senior claims. Net ending assets equal remaining portfolio value after any loan liability. Ending net portfolio value is shown for easy comparison. Tax effects are noted qualitatively.

Key Takeaways from the Scenarios

The scenarios demonstrate how each strategy responds differently to market conditions. In moderate declines and flat markets, the STRC mixes preserve substantially more capital than the loan approach. Even in a strong 50 percent Bitcoin rise, the standard STRC mix delivers the highest ending net portfolio value while the higher-cashflow version matches the loan exactly. In the extreme 80 percent drawdown, the loan strategy results in total loss of the portfolio through liquidation, whereas both STRC mixes retain meaningful value despite the additional decline in the STRC portion. In a 500 percent Bitcoin rally with total STRC collapse, the loan strategy captures the largest upside due to full Bitcoin exposure, while the STRC mixes still deliver cash flow during the year but end with lower portfolio values. Tax treatment further differentiates the approaches: loan proceeds remain non-taxable, while STRC dividends provide ongoing tax-deferred cash flow.

Bitcoin-backed loans

Pros: Larger immediate cash availability and full exposure to Bitcoin’s upside in rising markets.

Cons: Interest expense creates a steady drag, the outstanding principal requires repayment or refinancing, and full exposure to Bitcoin's downside reduces net equity more dramatically while introducing liquidation pressure that can result in total portfolio loss.

BTC + STRC mix (standard or higher-cashflow allocations)

Pros: Recurring cash flow without debt service or repayment obligation, built-in price stability on the STRC portion, stronger capital preservation when Bitcoin falls or stays flat, and tax-deferred dividends. The higher-cashflow version increases monthly income to better match larger expense needs.

Cons: Smaller annual cash amount than a loan in the standard mix and reduced participation in strong Bitcoin rallies (especially in the higher-cashflow version).

Which Approach May Be Right for You

Choose a Bitcoin-backed loan if you need a significant one-time or flexible amount of cash right away, remain bullish on Bitcoin’s long-term price, and can comfortably manage interest payments, monitor LTV levels, and plan for principal repayment or refinancing. This approach suits businesses with seasonal cash needs or individuals who want maximum Bitcoin exposure.

Choose the BTC + STRC mix if you prefer steady monthly cash flow, want to limit downside volatility, and value principal stability on part of the portfolio. Use the standard 75/25 allocation for balanced growth and cash flow, or shift to a higher-cashflow mix (such as 60/40) when greater USD income is the priority. This option often appeals to retirees, conservative family offices, or businesses seeking predictable expense coverage without adding debt to the balance sheet.

Many investors combine both tools or adjust allocations over time as their needs or market views evolve.

Conclusion

Bitcoin holders no longer face a binary choice between selling their Bitcoin or going without cash. There are stark differences, benefits, and risks of posting your own Bitcoin as collateral for a loan, versus purchasing a preferred equity or other credit instrument. Bitcoin-backed loans and STRC each represent practical, Bitcoin-aligned innovations that let individuals and businesses meet real-world financial needs while continuing to hold and accumulate Bitcoin. The right tool depends on your liquidity requirements, risk tolerance, time horizon, and market outlook. Retirees may have different needs than those with exogenous income. As the Bitcoin financial ecosystem matures, these and future options will give more people the flexibility to participate fully without compromising their core conviction in Bitcoin itself.

This article is for entertainment and educational purposes only. It is not financial, investment, or tax advice. Consult with a qualified financial advisor, tax professional, or legal expert before making any investment or financial decisions.

Mathieu Agee - Founder, O21 Solutions